Housing Bust #2 Has Begun – WOLF STREET

THE WOLF STREET REPORT

Imploded Stocks

Banks

Brick & Mortar

California Daydreamin’

Canada

Cars & Trucks

CRE

Companies & Markets

Consumers

Credit Bubble

Cryptos

Debtor Nation

Energy

Europe

Federal Reserve

Housing Bubble 2

Inflation & Devaluation

Japan

Jobs

The housing market in the United States has turned down, and in some big markets very dramatically so. Other markets lag a little behind.

That’s how it went during the last Housing Bust, that I now call Housing Bust #1. During Housing Bust #1, Miami, Phoenix, San Diego, Las Vegas, etc. were a little ahead; other places, like San Francisco were a little behind. In 2007, people in San Francisco thought they would be spared the housing bust they saw unfolding across the country. And then it came to San Francisco with a vengeance.

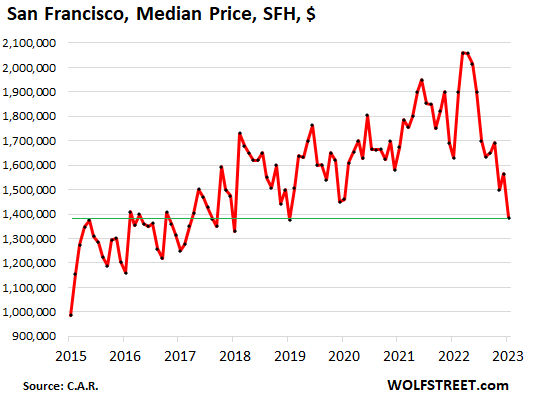

This time around, San Francisco and Silicon Valley, and the entire San Francisco Bay Area, are at the forefront, along with Boise, Seattle, and some others. In the San Francisco Bay Area, during the first 10 months of this housing bust, Housing Bust #2, the median house price has plunged faster than it did during the first 10 months of Housing Bust #1. That’s what we’re looking at. I’ll get into the details in a moment.

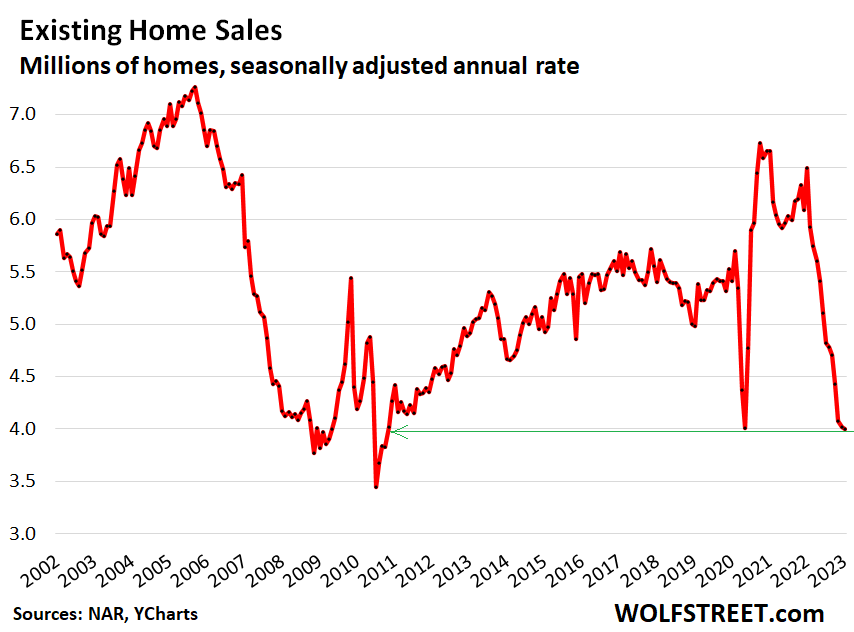

Across the US, home sales have plunged month after month ever since mortgage rates started to rise a year ago. In January, across the US, total home sales plunged by 37% from January last year. Sales plunged in all regions, but they plunged worst in the West, by 42% year-over-year, and the least worst, if I may, in the Midwest, by 33%. This is happening everywhere.

The median price of all types of homes across the US in January fell for the seventh month in a row, down over 13% from the peak in June. Some of the decline is seasonal, and some is not.

This drop whittled down the year-over-year gain to just 1.3%. At this pace, we will see a year-over-year price decline in February or March, which would be the first year-over-year price decline across the US since Housing Bust 1.

Active listings were up by nearly 70% from a year ago, though by historical standards they’re still low. Lots of sellers are sitting on their vacant properties and are holding them off the market, and are putting them on the rental market or are trying to make a go of it as vacation rentals. And they’re all hoping that “this too shall pass.”

“This too shall pass” – that’s the mortgage rates. The average 30-year fixed mortgage rate went over 7% late last year, then in January, it dropped, went as low as 6%, and the entire industry was breathing a sigh of relief. This was based on fervent hopes that inflation would just vanish, and that the Federal Reserve would cut interest rates soon, and be done with this whole nightmare.

But in early February came the realization that inflation wasn’t just going away. Friday’s inflation data confirmed that inflation is reaccelerating, that it already started the process of reacceleration in December. Some goods prices are down, but inflation in services spiked to a four-decade high. Services is nearly two-thirds of what consumers spend their money on. Inflation is very difficult to dislodge from services. The Federal Reserve is going to have its hands full dealing with this – meaning higher rates for longer.

And mortgage rates jumped again and on Friday were back to about 6.9%, according to the daily measure by Mortgage News Daily. Just a hair below the magic 7%.

And potential sellers are still sitting on their vacant properties, thinking: and this too shall pass.

So how many vacant homes are there? The Census Bureau tracks this. In the fourth quarter last year, there were nearly 15 million vacant housing units – so single-family houses, condos, and rental apartments. That’s over 10% of the total housing stock.

In 2022, the number of total housing units increased by over 1.3 million. If each housing unit is occupied on average by 2.5 people, that’s housing for 3.3 million more people than in the prior year. The US population hasn’t grown nearly that fast in 2022.

Ok, so now here are nearly 15 million vacant housing units. Of them, 11 million were vacant year-round. Some of the 11 million were being remodeled to be rented out, and others were for sale, and that’s the inventory we actually see, and there are other reasons why homes were vacant.

But 6.6 million homes were held off the market, for a variety of reasons, such as that the owners don’t want to sell the property at the moment.

If just 10% of these 6.6 million homes that are held off the market show up on the market, it would double the total number of active listings. If 20% of these homes show up on the market, it would trigger an enormous glut.

This is the shadow inventory. It can emerge at any time. And during Housing Bust 1, this shadow inventory that suddenly emerged created the biggest housing glut ever.

Since the San Francisco Bay Area is ahead of the game, let’s look at it more closely. It’s a market with a population of just under 8 million people. The median price of single-family houses in January plunged by 35% from the crazy peak in April last year. Year-over-year, from January to January, the median price has plunged 17%. This is according to the California Association of Realtors.

In dollar terms, the median price plunged by over half a million bucks from the peak. That’s a lot of money to go up in smoke.

Well, it’s not really money that went up in smoke, it’s the illusion of money that went up in smoke.

Prices had spiked so fast during the free-money era of the pandemic that this massive plunge didn’t even take the price back to January 2020.

Not that many people bought a house during these three years, and fewer still bought a house near the peak. So the plunge in prices didn’t actually impact a lot of homeowners – just those who bought after mid-2020. That’s a relatively small number. The homeowners who bought in 2019 and before, that’s the vast majority of homeowners – they are still above water, and many of them are still sitting on a lot of equity.

But this thing is moving fast now.

During Housing Bust 1, over a two-year period, the median price in the San Francisco Bay Area plunged by 58%. Now, we’re 10 months into housing bust 2.

So over the first ten months of Housing Bust 1 back in 2008, the median price plunged by 21%.

Over the first ten month of Housing Bust 2, in 2022 and 2023, the median price plunged by 35%.

In other words, the median price is now falling faster than it did in 2008.

Granted, median prices are not the most reliable measure. They’re very volatile and they’re seasonal. And they can get skewed by a change in the mix. For example, if the rich pull their homes off the market because they can afford to hang on to them, and only mid- to lower-end homes are sold, then there are fewer high-end homes in the sales mix, which pushes down the median price. This happened during Housing Bust 1, and was a factor in the 58% plunge in the media price.

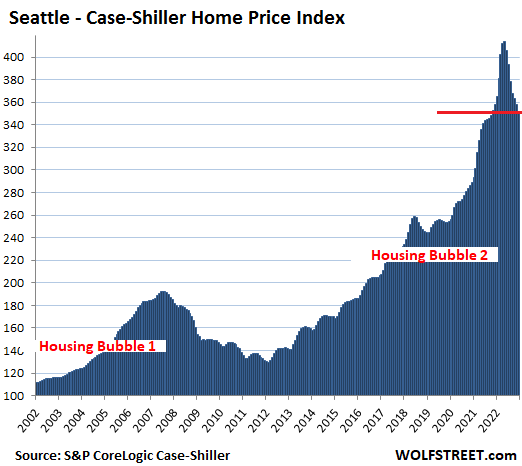

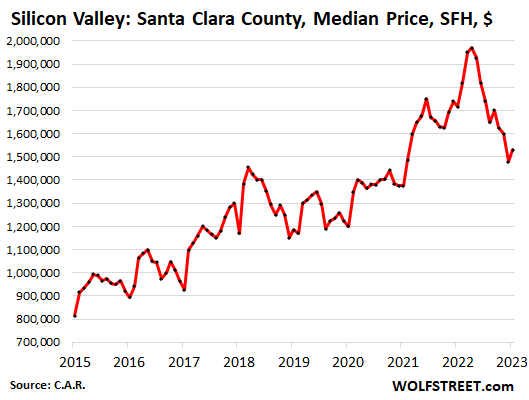

There are other markets that have home price declines that are similar to those in the Bay Area, including Boise and Seattle. But other markets just started turning down.

In the Bay Area, home sales – so the number of sales that closed – collapsed by 37% year-over-year, which is just above the national average of 34%. This is the sign of a frozen market.

Active listings have jumped in the Bay Area, and days on the market have nearly tripled from a year ago, to 32 days.

Pulling the home off the market is now a common practice. What lots of sellers are now doing is that they list the home at some aspirational price, and no one shows up. A month later, they pull it off the market. A month later, they list it on the rental market to see if they can get someone to fork over enough in rent to cover the mortgage payment. And that obviously doesn’t work. So then a month later, they pull it off the rental market. And then another month later, they relist it for sale at a lower price. Others are trying to make a go of it as a vacation rental, but there are tons of vacation rentals all over the place, and it’s hard to make that work.

If sellers cut the price enough, eventually the home will sell. If the price is right, anything will sell. The clearing price is reality. The hard part is for the seller to accept the clearing price, if they can actually afford to sell at the clearing price.

Some sellers put the home on the market priced right from the beginning, and they make a deal quickly.

For sellers, this is not the time to dilly-dally around. If they do dilly-dally around, they’re just going to chase prices lower. Those who panic first, panic best.

It’s not like there is no market out there, and no buyers. There is a market and there are buyers, but the market and the buyers are just a lot lower than where they used to be.

So why is all this happening so fast?

It’s not the economy. People are working, their pay has gone up by the most in four decades. Unemployment is still near historic lows. Actual layoffs and involuntary discharges – meaning people getting fired – are near historic lows.

Even during the Good Times, there are on average 1.8 million layoffs and discharges every month, and that’s part of the normal churn in the huge labor market. Every month for the past two years, including late last year with all the layoff announcements hailing down, the total actual layoffs and discharges were below the Good Times lows before the pandemic, they were at 1.5 million a month or below, the lowest in the data going back over two decades.

Unemployment goes up when there are more of these layoffs, while companies stop hiring, and those that got fired or laid off suddenly can’t get a job any more. And that’s just not happening yet.

Companies have hyped these layoff announcements for months. Usually their stock price jumps when they do. But they’re just announcements, not actual layoffs, and they’re by global companies for their global staff, and many of those layoffs take place in other countries.

Actual layoffs are easy to check in California because companies with more than 75 employees have to report them under the Worker Adjustment and Retraining Notification Act.

San Francisco was the worst off with layoffs, in terms of the size of the labor market. But it only had 7,000 total layoffs since July, despite all the hoopla about the 5,000 layoffs at Twitter alone, and the tens of thousands of layoffs at a bunch of other companies that are either headquartered in San Francisco or have big offices in San Francisco.

And that was as bad as it gets in California. But other companies are hiring, and in California overall, employment has still increased. And the unemployment rate is still historically low.

In other words, there just isn’t a surge in unemployment. The labor market remains tight. People are working and they’re getting big pay raises, and many of those that got laid off are finding new jobs quickly. And that should be great for the housing market.

But this housing market didn’t get tripped up by a surge in unemployment, not even in the Bay Area. Unemployment is a shoe that might drop on this housing market in the future.

What tripped up the housing market so far is the toxic mix of several factors, including:

Home prices had exploded into the stratosphere because of the Federal Reserve’s monetary policies – and nothing else – because of the nearly $5 trillion it printed between March 2020 and March 2022, to repress long-term interest rates, including mortgage rates, and to create the biggest asset price bubble ever.

But now all this is over, now we have raging inflation, the Fed hiked rates, and will hike them further, they will go over 5%, and the Fed is pursuing Quantitative Tightening, and by the end of February, it cut its balance sheet by over $600 billion.

So the Fed is hiking rates and unwinding its balance sheet, and asset prices have come down, including stocks and bonds and cryptos, and housing.

What we’re seeing is the unwinding of the biggest asset bubble ever – including home prices. And so far, this has nothing to do with unemployment or the overall economy. Jobs are plentiful, wages are up, consumers are spending, companies are spending and investing, governments are spending like there’s no tomorrow.

This could change: Unemployment might surge, and job openings could vanish, and consumers who lost their jobs could cut back on spending, and state and local governments that are still swimming in pandemic money, will run out of this pandemic money and then they will have to cut spending. All this is the other shoe that could still drop on the housing market.

But it hasn’t dropped on the housing market yet. The decline in the housing market so far has been driven entirely by the rapid disappearance of free money that everyone had gotten used to since 2008. Housing Bust #2 may turn out to be a sobering trip from the free-money decade in la-la-land, back to normal.

You can subscribe to the podcast of THE WOLF STREET REPORT on YouTube or download it wherever you get your podcasts.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.![]()

Email to a friend

The Housing Bust 2 may be starting in the San Francisco Bay area but it is not reflected in the price of SFH’s and Condo’s yet. I’ve lived in SF for 20 years and make about $115/hr and there is no way they I have ever felt that I could afford to buy a residence large enough to feel comfortable living in. Meaning, over 800 sq feet, with parking and laundry in my home. Homes less than $1,000,000 are few and far between, in the hinterlands or a dump. All of the properties have been snapped up by wealthy hedge funds or foreign money. I have not seen anything change in this regard, so far…

You can get a pretty decent condo for $1 million or a little less, with 900 – 1,600 sf. New construction too.

Median condo price is $990k, meaning that HALF of the condos that were sold in January sold for less than $990K.

Zillow lists 289 condos for under $1 million.

“In other words, the median price is now falling faster than it did in 2008.”

Woohoo! Keep it up! But the cold hard reality is that, save 7 or so markets, the rest of the US is NO WHERE NEAR 2008 – 2010. It’s that simple. And we won’t arrive near or pass those levels of broad, national decline without a massive pickup in unemployment. 190K 1st time unemployment claims is rock bottom. It’s as if there’s literally been zero layoffs.

Yes, the economy is reaccelerating which means the 450 basis points rise to the FFR hasn’t cut it. Granted, history tells us it may take another 6 months for the FFR to really percolate through the economy. As such, the Fed continues to slow roll FFR increases. Given the current data, we should be at 600 basis points with the real possibility of 700 starring us down the barrel of the Fed’s loaded gun.

A measly $38B in loses. And like you say, the Fed can’t go broke and their current dot plot isn’t pushing core PCE inflation down to 3% anytime soon. If inflation rises through the summer, we all had better get ready for a 7-8% terminal FFR. Every month the Fed adjusts it’s dot plot upwards with no real handle on what the actual terminal rate will be.

What’s really needed is a 25% drop in the stock markets ASAP which would really effect people’s net worth and willingness to let these price increases continue. I’m ready to go. 90% of my money is in brokered CDs.

the real problem is lots of those californians moved to Arizona

and doubled our housing prices

I have better than 97% occupancy in rentals

and over 1/2 homes selling today are CASH

I’m buying and estate sale at 1/4 california price

not sure if I’ll flip or keep as rental

either way I make better than 15% ROI

mortgage – so sorry I just pay cash

“I’m buying and estate sale at 1/4 california price”

Hahaha, what kind of market is that where you can buy a house at 75% off?

called Arizona

Estate sale sounds like ‘distressed’ real estate… 1/4 of 1M+ would go a long way in some areas and with some houses.

Is this a slumlord type situation?

Thanks Wolf, you are correct as usual. I think my point was missed and I should have been more specific. The median Condo price is $990K.

My point was that I a “blue collar”, hourly wage earner making around $200,000/year cannot afford to own a $990K home. There is no way I can even save the $90K for a down payment in less than 20 years. I spend $3,100/month on rent alone. Right now in San Francisco you need to have inherited property/money or have a job paying 300K/yr to afford to own a home. Unless you find a “good deal” which will most likely be a dump or in the hinterlands. Hedge funds and foreign investors snap up the housing stock to rent or just let it sit empty. I have heard for at least 10 years, build build build will bring prices down and make it “more affordable”. Thousands of these home have been built and the price has not come down. I do not qualify for any assistance from the City because I make too much. For me it looks like I will forever be a renter. Unless the median price comes down at least another 33% to around $600K. So as I see it, the 2nd housing bust has come not to me but the Hedge funds and wealthy investors.

Jas, your take home is what.. around 150-160k a year? and 40k goes to rent. How are you not able to save 90k in a span of several years? Where’s the rest of the money going?

Even if you max out 401k contributions you should be able to save enough each month to make a considerable downpayment

Your experience makes no sense to me. I lived in The City from 2000-2011. Started with a combined income of 69K in a one bedroon (700 SQ ft). at $1650 in lower pac heights rent controlled apartment. Got the rent reduce in 2003, thank you dot com bust and probably could have done the same in 2011 but we left. Rent control meant rent increased 2% a year max We never made more than 100K and averaged 85K but we were still able to save more than 10% down on 750K by the time 2010-2012 rolled around and prices bottomed from the GFC. We would have easily afforded a one bedroom in lower pac heights and if we were willing to go to ( at the time) mission bay, potero hill, outer sunset, outer mission, diamond heights, bernal heights, Bayview, hunters point, the Richmond, or many other neighborhoods we could have afforded a two to three bedroom condo.

Not saying it didn’t happen to you but I am saying it was possible with the appropriate actions to save and afford a property in that time frame with your salary in The City.

I have to concur with Troy, you must have some other expenses if a 200K salary can’t get you into a 900K home. To compare, I’m using CAD but for this comparison it’s fine to use 1 to 1. My salary last few years averaged about 80K, last year I moved up to just over 100K. My current rent is 1600/Month, it’s less than other places because I moved way out in to the burbs of Vancouver and stayed put, this allows me to save but I pay for it in commute time, prior to that I put in a hard year and a half in a total dump for 800/month, it was an awful place but I saved a lot. Few yrs ago me and a buddy split on a fixer upper, 1yr later and 25K in material we sold it for a marginal profit. Right now I have a modest car, cost 32K (in Canada everything is more) paid for in cash and 110K sitting on the sidelines, I’m waiting and hoping for prices to come down.

It’s all doable but unfortunately requires some sacrifice, if I made 200K/yr in tech I’d be laughing right now. But I do feel your pain, 900K is a lot for just a condo, but you guys get much better weather than anywhere I can get in Canada 😂

200K annual income is pretty handsome. If you’re having trouble saving, maybe get outta that overpriced ass’d city?

That said, my brother-in-law is a partner/contract lawyer and I think he makes shy of .5 a mil annually and even he groans about money; there’s maybe a lesson here…

But yeah, you probably shouldn’t be looking at a 900K house. I would think 750K would be max, which should afford you quite a spread. Me — I’d rather buy a restored land yacht and bank the difference.

And “the rest of the money” is probably going to stuff like insurance (health insurance alone is out of control). Maybe student loan debt? Some condos might appear affordable at first glance, until you factor in HOA fees. Then there’s property taxes, which are absurdly high in CA (unless you’re a boomer who lucked out with prop 13). 200k in SF doesn’t go far, which is wrong.

Take BART or find a cheaper place.

People take the ferry from Vellejo over every morning.

I knew a guy that repaired elevators that drove from Vacaville for like 30 years. (Not suggesting this btw)

Also, stop spending all your money 😉 Honestly, a lot of people blow $12k a year on restaurants and complain they’re “broke.”

Jas, Is this one more fake post from a frustrated realtor to claim that all real data posted here is shit and that housing never goes down.

If yes, you guys have already fooled a bunch of first time buyers during Pandemic who are depressed to find that their houses are already down a years salary and 3 years savings!

In Seattle, with price falling ~2% every month, buyers are saving ~ $20K every month on a million dollar house for a full cash purchase. Add the 30 year 7% interest to that $20K, and it becomes $48K savings for every month they delay buying the house.

That’s more than thrice the earning of most households in this region.

So while there has been corrections, this is still NO TIME TO BUY.

Jas is correct, just look at Zillow. The condos below 1M are mainly 1b/1b 800 sqft.

And a new construction price on Zillow doesn’t reflect the price you pay. I bought several new construction houses and you always end up more than what they advertise on Zillow.

In general, a lot of the FUD currently is fooling people into thinking we have another 2008 coming. It’s far from true. But wait and see yourself.

Tavor, In Seattle, with price falling ~2% every month, buyers are saving ~ $20K every month on a million dollar house for a full cash purchase. Add the 30 year 7% interest to that $20K, and it becomes $48K savings for every month they delay buying the house.

That’s more than thrice the earning of most households in this region.

So while there has been corrections, this is still NO TIME TO BUY.

Leo,

I would love to see your data resources that can show the -2% every month in the Seattle market.

Being an investor, I’d be all over that market.

However, I’m also a real estate broker and have access to the actual MLS data and it tells me a different story:

City of Seattle:

Average Sales Price

Days On Market

Average Sold To List Price

Average Price Per Sq. Ft.

If there’s other data that you’re interested in, I’ll do what I can to provide.

Coach Jim,

“average sales price”???? Really? You’re out there citing “average” price? Average price is absolutely the worst measure. I deleted all of the links to your thingy.

So here is the Case-Shiller which lags behind, for the Seattle metro. It is based on “sales pairs,” meaning it tracks the price of the same house when it sells in the current months to when it sold previously. This is the most accurate measure of home prices we have, but it lags. The median price is not nearly as reliable but it’s still a decent measure. Average price is absolutely the worst because it gets skewed by a few outliers.

So per Case-Shiller, in the Seattle metro:

Month over month: -1.8%.

From the peak in May: -15.1%.

Year over year: -1.8%.

Lowest since October 2021.

Nobody can time the market. When Covid hit people said we will enter a depression. The worst thing you can do is buy a house. Well I did and it worked out beautifully. I got lucky! Super lucky. I had no idea that the market will take off like a rocket.

I bought because we could comfortably afford it and I wasn’t too worried about prices dumping because I planned on staying in this house long term.

Fast forward 1-2 years and people said the forbearance tsunami is coming. A wave of foreclosures! People were wrong again.

Fast forward and interest rates are skyrocketing. Another 08 type drop is coming! Are the FUDsters right this time?

I believe it when I see it 🙂

@ Coach Jim

Beyond the charts provided there is no way to avoid the simple math. Borrowing costs have gone from sub 3% to now 7% and climbing. The rule of thumb is that each 1% of rate increase correlates with a 10% drop in purchasing power – meaning a 10% drop in sales price.

And you seriously believe that residential will hold it’s value? No one’s buying your take. As an “investor” now is the time to sell.

Good luck

@Tavor said “I believe it when I see it :)”.

Why doesn’t Tavor see the 15% drop in Seattle case shiller index over 7 months from peak?

Oh yes, being a “RE investor”, his survival depends on spreading misinformation to help find a bag holder for his shit.

It’s a tough business to be in today. I would give Tavor my best wishes, but it won’t really matter.

Tavor,

#1. Your statement about condos in SF — “condos below 1M are mainly 1b/1b 800 sqft” — is BS. You didn’t even look at Zillow it seems. Or you looked and lied. There are 169 condos with 2 or more bedrooms below $1 million listed for sale right now on Zillow. That’s a huge number for a small expensive market like SF.

46 of those 2-bedroom+ condos are listed below $700K.

#2. You’re hyping RE so that people will buy so that prices stop falling and start rising again because your wealth depends on high home prices and high rents, as you explained many times. So that’s your point of view, and it makes sense from your point of view because your wealth depends on it. And you’re trolling these comments to help promote your wealth (or perhaps you’re just a paid RE troll).

Others look at this chart and think it’s better to be patient, very patient, before buying and thereby putting a stop under the plunge and bailing out people like you, LOL

If you’re not patient, you can lose $500k in a hurry. Some people already have, as you can see:

“46 of those 2-bedroom+ condos are listed below $700K.”

And I don’t care where you live. $700K for a 2 bedroom, run of the mill condo is still very overpriced.

EVERYTHING is still overpriced, including SFO! Prices have to fall 50% just to wipe out the 3-4 year gains prior to May 2022.

“EVERYTHING is still overpriced, including SFO! Prices have to fall 50%…”

I totally 100% agree. Long way to go. Falling knife… We just started. You gotta be patient with housing. It’s not crypto. Housing Bust 1 took 4-5 years, amid massive money-printing spree and interest rate repression.

Now we have inflation, QT, and rising rates. The 30-year fixed is at 7%. Totally different ballgame: No money printing, no interest rate repression.

BTW, “SFO” is the airport. The rest of San Francisco is SF or San Francisco or whatever. But not “Frisco” which is a city in Texas.

“no interest rate repression”

With Fed Funds still around 8-9 % below the actual inflation people are actually experiencing ?

I guess I don’t agree .

Thanks Wolf for taking time to replying these real estate pumpers.

I see this particular article touched a lot of people invested in real estate in a wrong way 😳

“46 of those 2-bedroom+ condos are listed below $700K.”

Sounds low, honestly… do those include BMR listings with income limits? TICs where you are in some weird contractual arrangement with the other owners?

It’s high compared to how few there were a year ago.

No.

TICs (Tenancy in Common) are a very small number. Just a few sales each month. There are three legal ownership models in SF: condos, co-ops, and TICs. Look up the legal differences.

Already looks 08ish in SF, which I think is the point of the article.

Will it 08? Less? More!?!

No one knows. What happened in housing is rare here in the states. It might be just a shitty investment for a while. It might be a crash.

But housing looks fucked to me. Not Japanese asset bubble fucked, thankfully, but not somewhere I am looking to invest for a long term horizon expecting a return. And if just looking at housing for consumption, rents and putting your money elsewhere seems like better returns in a world of cash at 4-5% for a while.

Jas

Don’t be too emotional and rely on anecdotes.

Just follow the data and you’d see things clearly .

Thanks to WR for these data.

warning to anybody who is tempted to comment before a careful reading. please carefully read the above before posting. I’m tired of Wolf having to school errant children who insist on opining with their usual schtick, and then Wolf has to put on the Iron Glove. It’s always uncomfortable and embarrassing for the flock.

I bet you were teacher’s pet.

Jas may be socaljim / kunal under new names: “Here in socal, Sun never sets on the housing markets …..”

brilliant post.

I listened to the podcast version of this post so I’m guessing that doesn’t count?

Freedom of speech should always be honored just in case something was misunderstood or misinterpreted by anyone. Wolf decides,it is his sight.

If Wolf decides to have an “AI” algorithm to sensor certain topics that is his business, or if he just decides on his own.

For instance, instance certain subjects arfe off limits, and comments are removed without discussion.

Regardless, I still like the sight, but wish cetain subjects were allowed to be discussed. The pandamoneum pandemic messed things up.

cite==sight

…site…cite…sight…(…think i’d have a lot more trouble than I do with the ‘Murican tongue were i not a native speaker. Wolf, as usual, shames most of us in that regard…).

may we all find a better day.

site==sight. cite site. Site – location, Website. Cite – to quote something.

Agree. Freedom of speech is a right, but it’s not valuable when people make statements that are clearly biased or unsupported by facts.

There’s a lot of garbage on the internet. I think Wolf screens 90% of this out, but he lets some of it get through so we can watch them get taken behind the woodshed. It’s good humor.

Jas and Tavor, what’s it like in the after-world?

“It is difficult to get a man to understand something, when his salary depends on his not understanding it.” ― Upton Sinclair

Unfortunately, we’ll have to slog thru that crap till we hit bottom many years from now, at which point we’ll hear the “see, I was right!” posts from these same sales-clowns.

Hey, everyone has to eat, and some paychecks are dependent on lies to generate those sweet commissions.

+1

May-Day 15/2023?

@ Phil – I feel the same way. And Wolf seems so tired of that so he usually calls every such comment a BS or a lie – which also feels embarrassing.

I dunno I like the chatter. For example, the obsessive denialism helps give a feel as so many folks are talking their books and are leveraged long in RE.

Herd hasn’t spooked yet. Otherwise we’d see more anger at the banks, the Fed, the government for getting them into houses by “tricking” them with low rates for a decade.

I dunno. I kinda enjoy it in some sadistic manner.

$115/HR. I’ll take it. Thank You.

Everyone have a great weekend. 😂😂

$115HR is good money in a state with no income tax, like FL or TX, but in CA or NY where the overall tax rate can be over 50%, it’s living paycheck to paycheck money. I know from experience.

$115/hr and living paycheck to paycheck!!

We are a very diverse country.

Love your response!

If you’re living paycheck to paycheck on 115/2=57.5 an hour take home, you have bigger problems than not finding a 2bd condo to your liking.

Most people don’t have an in-come problem, they have an out-go problem.

$57/hr sole income pre-tax in NYS is absolutely paycheck to paycheck from NYC straight up the Hudson. Some of us manage on less, but it requres serious thrifting, home haircuts and foregoing retirement savings. God I loathe this state.

Post tax, eh, you’d be fine if you stopped keeping up with the Jones’. Time to trade in the BMW for a Toyota and lose the unused fancy gym membership.

I’m with you. But don’t diss “home haircuts.” I think mine looks pretty good and I like doing it. There is something very satisfying about handling a power tool.

Lily: It’s $57.50 an hour AFTER taxes (if taxes eat 50%).

Sorry. @ $2300 a week…. $10K a month (fuzzy maff) is not po’ boy money.

We do a lot better on a lot less. Our fixed monthly income (not the variable part) is a similar amount…. and we don’t spend nearly half of it (and we deny ourselves not much… just stupid stuff). When the Jones’ can’t keep up with themselves…..

If you can’t save on $10K a month, someone has a spending problem.

Home haircuts the way to go. If you know how to prune a shrub or manipulate/sculpt reasonably well in any medium you can sneak by ok with a patience and some proper shears. Women’s hair is a different story, and usually benefits from the finesse of a seasoned coiffurist.

It’s always the classic no state income tax mantra. Before anyone crows about low tax Texas, please check out the sales taxes, the gigantic property taxes and the huge homeowners insurance rates. A regular house for sale now in San Antonio: $1706 a month for property taxes and $445 a month for insurance. That’s a total of over $25,000 a year. Sales taxes will nick you for another $5K to $8K a year. That doesn’t even take into consideration the utility bills: 59 days over 100 degrees last year – maybe 65 this year and getting hotter every year.

Thank you Escierto, been saying this a while, as much as we love about Texas it is absolutely not a low-tax state, that’s got to be one of the biggest marketing myths pushed by any state in decades. Texas property taxes can be crushing in many districts, some of the highest in the US and they cause a lot of pain to families because it’s not like your home value is a liquid asset you can use as an ATM to pay off those assessment taxes. Travis and Hays counties (Austin) are notorious but the drift in property taxes has gotten bad across the state, even in the rural towns with more cows than people. I’ve worked in a lot of states and have family in others and it’s probably only a couple states, maybe New Jersey and one or two in New England that have a heavier property tax burden than Texas. Then there all kinds of hidden licensing fees, surprisingly high business taxes and the effective taxes from things like speeding tickets can be brutal. And if you get divorced in Texas you’re likely to lose your shirt especially if you’re a doctor, executive or other high-earner because it’s a money-maker for the state and the divorce courts make sure to impute your costs as high as possible. (Though being fair that’s true for most US states, might as well go expat if you actually want to get married and have a family, most countries don’t see divorce as a profit center)

It’s just funny how even as polarized as America is, one of the few things left and right supposedly agree on is that Texas is some kind of idealized right-wing haven, when in fact Texas cities and urban culture are probably some of the most diverse and progressive in the US and on economic policy, if they actually looked at Texas taxes and esp the property tax most conservatives would scream it’s more socialist than Sweden, if not communist. (And Sweden for that that’s worth doesn’t even have a bad property tax burden, most of the EU is lighter than the US on that especially for a primary home and taxes are more limited to point of sale and investments–one of the ways the whole claim of “lower tax USA” in general is a myth) And you’re right about the utility bills and homeowners insurance too, Texas really is following closely in the footsteps of California despite all the ways it tries to say it’s different. A big irony now with a lot of the California transplants getting buyers remorse and realizing they came out of their frying pan and into a fire that dredges up a lot of the very things (housing bubble, high taxes, awful traffic) they thought they were leaving.

The same property taxes and insurance in FL and they are rising.

Texas property tax are, for a southern state, insane. When my son moved from Tampa to Texas for work I was excited, getting tired of Florida, so I thought I might follow.

Nope, the average property tax is double that of a Florida resident, even more if your Florida Homestead.

Insurance is the killer in Florida at the moment. No reason to think DeSantis will fix it. Crist didnt, Bush didnt, Scott didnt…….

I’m hoping it slows the Blue state Yankee tide lol.

…seems that a Master Berra event horizon may be approaching in other areas…

may we all find a better day.

“Always go to other people’s funerals. Otherwise they won’t go to yours.”

Holy baloney. $115 an hour could mean many things. W2 wages? 1099 wages? Contracted wages through an LLC/S-Corp?.

Assuming $115 an hour W2 wages, that’s about $230K per year converted to 40 hours per week. In San Fran, that may not be a lot money for someone who is constantly spending money on restaurants, ordering takeout 3-4 nights per week, car payment, rent, vacations, etc. I would call it decent money in San Fran and combined with a spouse who makes the same or even half of that, then it becomes comfortable money in my mind. Everyone is different. I know people making $300K in Texas as a family of 4 and living paycheck to paycheck BY CHOICE.

We all make choices. Jas CHOOSES to live in San Fran. Most people focus on the money coming in, but the most important part is the money coming out.

As a bay area native, and having been an hourly worker for most of it, I find the number of $115 to be an oddity. In my experience, when I started to earn over $60/hr at any company, they usually just bumped me to salary. As it stands now, I’m “skilled labor” doing very technical welding work, and of the type of industries available in SF, I can only think of one place that might pay an hourly worker $115/hr for their time without a full benefited salary role. Heck I was just recently offered a job in with the title “space welder” that didn’t pay half that number. Something seems fishy with story.

It’s 2023. 115 is the new 60.

He did put “blue collar” in quotes. Maybe IT work of some kind?

Wolf, you’ve been using the phrase “back to normal,” paired with “biggest asset bubble ever.” I’ve lived through a few of the prior busts in my 74 years. I know you don’t have a crystal ball, and I asked this a week ago on an earlier housing post… Don’t you expect a period of “below normal” before “back to normal” returns?

Make no mistake, I not only want to see back to normal, I’m expecting it. And by that, I mean the end of the ultra-wealthy raking in gains while working people suffer. My vision of normal is a thriving middle/working class. I think it’s incoming, but there’s going to be some damage before Main Street entrepreneurs start outperforming Wall Street gamblers again (as they certainly should and will)….

Hi Laurence. I’m 71. IMO “normal” is not returning in my or your lifetime. Hunker down. May we all find a way to fulfill our remaining days with enjoyment every day with family and friends. Go hiking. Go hunting. Go fishing. Best of luck.

My take, normal will not return in dollar terms as dollar is falling like a brick (high inflation). We should return to normal when corrected for real inflation rates because, QE is no longer possible without hyperinflation.

When will normal return? Inflation remains stubborn and frustrations will start peaking soon. Corrections are steeper than last time and will actually pick up pace. So I fell its only 1 to 2 years to an inflation corrected normal that may not be the bottom due to systemic and political risks.

“QE is no longer possible without hyperinflation.”

Actually I’d love to hear about this take in more detail. I’m not schooled in economics. My understanding so far is that after ’08 we saw massive asset price inflation and growth in wealth inequality because most or all the money went to the wealthy, a lot of pandemic relief money went to the public and now we have inflation in goods and services. Or is it that we are now dealing with fallout from ’08 QE but only now is it showing up in CPI and CPE and stuff?

People have been predicting hyperinflation for the past 50 years.

Seba,

I think the quickest summary is this –

1) For a far too long time, DC used its money printing power to artificially drive interest rates *far* lower than they would otherwise be (DC did this by printing money to buy its own and others’ debt),

2) Artificially low interest rates caused artificially high asset prices (via something called the Discounted Cash Flow formula) and in general unsustainable artificial demand in everything,

3) To offset pandemic impact, DC did 1 and 2 again, on meth.

4) Pandemic/Ukraine War/Dumbass computer chip fires caused supply chain disruptions that ignited real shortages/price spikes…hugely amplified by all that macro-economic meth that DC had been dealing for over a decade.

That’s pretty much it – we can step through the details but it would take a lot more time.

Seba: When you look at *real* vs official inflation numbers, and when you also consider asset inflation from 1980-82 to 2020-22, it’s in fact been hyper. That is, (1) you have to look at what we’re all really paying; and (2) the historically unprecedented run-up in asset prices mostly across the board.

Gomp, I’m 79 and “normal” to me is a daily bowel movement.

Other than that, I keep my head down and keep thinning the cabbage around here.

LOL LOL LOL 🤣🤣🤣

Very true

Its a matter of time when we all would seek this kind of normalcy 😀 no matter how much money or houses we own

A thriving middle class…

Well, we are seeing wages skyrocketing for the lower incomes but of course the rich made the most off the pandemic. This is a good example of trickle down economics in action. The rich go from making 100 million a year to 200 million a year, while the working stiff goes from 20/hr to 25/hr.

Hyperbolic? Sure. But it’s not far from reality. I don’t think the middle class is going to grow in size in the future. Let alone prosper. I guess we’ll see though. I think the golden age of the US is likely past us. Corporate power and money in politics is getting well out of hand. It seems like we’re regressing back to the days of robber barons. A lot of things are better than they were but 50-100 years down the road, I think the greed of the rich will choke whatever advances we make to the point that they’re window dressing.

But again, I’ve spent my entire 20s holding a steering wheel and jamming gears. That makes for a pessimist of British proportions.

There are two large classes reflected by two parties in this country. One class/ party wants to take money from the middle class and give it to the below middle class (welfare). The other party wants to deregulate business so the rich can fleece the lower and middle class. Either way. There is no middle class party that’s wants to tame welfare and hold big business to account. The result will be less middle class.

I got a great LOL from this comment. ‘Welfare’ in it’s traditional meaning is at it’s lowest level in history – this is reflected via the percent it supplies for actual costs: food stamps, Medicaid, assistance for housing, minimum wages, etc.

Meanwhile, if you are reading this blog and have not yet figured out how much the government, the Fed, etc. is subsidizing the billionaire class, there is nothing anyone can do to explain it to you.

I just looked it up. Approximately 35% of households receive “needs” based government support. And that doesn’t include Medicare or social security. I couldn’t find all government subsidies easily, but I bet it’s well over 50%

That’s the point of my original comment. Everyone at the top and bottom are on the take. There’s no where, no party, to run to for the middle class who just pay. You just have to pick one and hope they don’t do anything too stupid.

Well said.

I don’t agree

Both the parties want to make money for themselves and their friends but one party has the mask of no big government and encouraging entrepreneurship while other has the mask saying we care for people

But remember at the end of the day both parties are out to rape and pillage this country

One political party pays their middle managers – congress type persons — well to provide ”socialism” for the poor.

The other ”party” pays their middle managers to provide ”socialism” for the rich.

Been that way since the formerly conservative democratic party followed LBJ through the looking glass to become ”reactionaries” on the left, and then the republican party followed ronnie ray gun through that same portal to become reactionaries on the right.

Crazy upside down ”interesting world” we live in these days,,, eh?

I agree. The middle class has no advocate.

However, in my view, it doesn’t matter. The middle class will recover despite this, because it’s not about politics, it’s about market economics & capital investment in real things, and Main Street is where the free market works when all the financial engineers and central planners have wrecked everything else.

The democrats have more billiionaires than the Republicans. The only reason that the democrats are willing to hand out money to the poor is so they have money to buy more stuff from the rich. The rich people plan is to pile massive debt on the nation because they have no intention of every paying a large share of their income to pay off the bill.

When you look at the total gains of the superrich, both realized and unrealized, the tax burden is down around 3-4% of income, mostly because unrealized gains can accumulate for decades and never get taxed.

gametv:

The real rate the rich pay is another of my favourite topics, as I’m a flat tax advocate. Take the 17% idea that was going around many years ago. If we all pay 17%, no deductions, then your tax percentage doesn’t increase as you work harder and earn more (no penalty). On the other hand, the rich pay 17% too (no deductions).

We all just cough up 17%. The income tax form is one page. And no individual needs an accountant. Nor will the IRS require scrutiny of pages of deductions and exemptions. Fewer IRS workers, accountants and lawyers. more actual workers and producers. Less waste in total, by far….

I’m in my mid 40s. What we coin as being “normal” is a return to the economy of maybe the 90s? 80s?

In truth the only long period of sustained “normal” in the terms of how most people think of it is going back from about 1945 – early 1970s. The poor were gaining income faster than the wealthy, the middle class was huge. Taxes were much higher, regulations on financial institutions were much higher, and we didn’t have any boom-bust cycles.

People were also content with much less. Homes were far smaller, we couldn’t really load up on debt like credit cards, etc. You kind of had to live within your means.

I don’t think we in America are capable of going back to that. The dynamics of our system are so different that. Barring some kind of massive change in social mentality and massive regulations on financial institutions, it’s hard to imagine we won’t just keep repeating these boom bust cycles.

RE: In truth the only long period of sustained “normal” in the terms of how most people think of it is going back from about 1945 – early 1970s. The poor were gaining income faster than the wealthy, the middle class was huge. Taxes were much higher, regulations on financial institutions were much higher, and we didn’t have any boom-bust cycles.

As an 84-year old senior, I remember what happened in early 1970. First, due to the reckless money printing to pay for Vietnam, price inflation skyrocketed to an astronomical 2% (yes) which scared Nixon enough to slap on wage/price freeze which backfired big time.

Then in 1971, on the advice of Arthur Burns, he reneged on the Bretton Woods agreement and terminated the gold backing of the USD, thereby turning it (along with all other currencies tied to it) overnight into a worthless piece of engraved paper with zero intrinsic value (like the stock certificate of a defunct company) propped up by nothing but the coercive legal tender law (legalized counterfeiting) and this blatantly dishonest act was applauded by the Financial Media as “closing the gold window” as if it was an accomplishment (the favorite ploy of all crooks).

In those days a Big Mac used to cost around 50c, gas was around 20c/gal, an average family sedan around $3,500, a typical middle-class house in Florida was around $30,000 and gold around $100/oz.

Comparing them with today’s prices, it is clear that ALL nominal prices have gone up more than 10 times or, more accurately, the fiat USD with which prices are quoted has lost over 90% of its purchasing power due to monetary inflation which nobody ever talks about and this trend will continue without end like falling into a Black Hole . . .

A minor correction, in 60’s average gold price was around 380.

I price RE in terms of gold, so 70 oz is a historical normal for a “middle-class house in Florida”

Ulysses, your comment, “The poor were gaining income faster than the wealthy, the middle class was huge. Taxes were much higher, regulations on financial institutions were much higher, and we didn’t have any boom-bust cycles,” is partially true but largely wrong.

There was no time that income for the middle class was rising at a faster rate than the wealthy. What happened in the post-war period was that all three “classes” were gaining prosperity at about equal rates. Taxes were higher for the wealthy, but their wealth continued to grow as it had in the past. Wealth and income tracked pretty consistently for the middle and uper class. The massive shift happened with Reagan’s tax cuts. Then the income differential widened and has not stopped. The “boom bust” cycle, or business cycle has not disappeared and was boom and bust a long, long time. This isn’t new. It wasn’t created by the Fed to enrich the wealthy and impoverish the middle class, although there are a lot of paranoids that think so.

All domestic use of gold for the US dollar was ELIMINATED entirely in 1933 and the price of gold was fixed at $35 per ounce and stayed that way until around 1972 at which time the price of gold was allowed for float in the commodities markets and moved to around $100 per ounce.

I’m only 68 but I remember buying five McDonald’s hamburgers for a buck after school 20 cents each.

Every change begins with changes in social mentality. For better or worse. The words fairness, everyman, empathy and honesty no longer have the high values they had 60 years ago.

Not that the 1970s and before that didn’t have their own problems, but values have definitely changed. Greed and selfishness have become more socially acceptable, even in some cases valued highly.

Everything goes in cycles and I expect at some point this too will change. Historically it doesn’t change in an easy way, but who knows..

When I entered the automobile business (wholesale manufacturer side), you could do business on a handshake as most dealers were self made entrepreneurs.

Now? Don’t go into the room without an army of lawyers. The B-school frat boys destroyed that business and this country.

Remember the old joke of “what’s the difference between a dead snake and a dead lawyer in the road?” There’s skid marks in front of the snake. Ditto the B-school wunderkind.

I really don’t perceive that to be true. Greed is not in season, at least not with the younger switched on kids. In fact, there is a palpable tension growing between the shits and the grunts in the US.

The pandemic, future shock and the diminishing returns of working class compensation have all combined to create both a collective dissipation as well as a outward disgust for a system designed to harness the labor and output of the many for the few.

Laurence, I’m afraid ‘normalcy’ for the middle class is a thing of the past.

Labor participation, Corporate off shoring, sky rocketing national debt, social security/medicare on the brink.

With the baby boomers falling into retirement and millennials slowly entering in ‘life’ (having a home, getting married, having kids, getting a career job) the whole ‘economic engine’ is off kilter.

The government continues to band-aid it with government policy, but in the end the train is still heading for a brick wall.

ONE SAVING GRACE is that this is America!

IF you get out there, bust your a$$, burn the candle at both ends, manage your way through all of the B$, you can still prosper.

You can own a business, you can invest in real estate, Wall St., etc. etc., it only takes some education, OJT, drive, and the grace of God, but you can make a good life for you and your family still.

I’d trace this back to Alan Greenspan’s tax rate and interest rate cuts. Low interest rates mean people could afford more expensive homes due to lower monthly payments. This in turn causes higher demand. As the supply of homes can ‘t scale up quickly, this causes home prices to rise. This is Econ 101 supply and demand stuff.

Since then, the party got wild, and nobody wanted to stop it. Housing bust #1 was a wake-up call, but only the homeowners got really hurt. Once the foreclosures ended, houses were cheap for a time. However, low interest rates soon goosed home prices back up to pre-Bust #1 levels, so the speculators jumped back in and the party was on again.

Only now, when inflation due to pandemic weirdness reared its ugly head, are we seeing interest rates rise. This will cause much pain in the real estate markets for a long time, as people with underwater houses can’t afford to sell, and folks seeking to build new housing encounter the problem of higher material costs paired with lower house prices.

As long as the rich get richer at the expense of the rest of us, folks earning median salaries won’t qualify for loans to purchase median-priced homes. I’m glad I bought my home several years ago, have steadily paid down my mortgage, and have no need to move. I couldn’t qualify for a mortgage on it now.

“folks earning median salaries won’t qualify for loans to purchase median-priced homes”

I don’t get why people think a median worker should be able to afford a median home. Those two medians (worker and home) are entirely unrelated. The median salary worker is, by definition, in the middle of the distribution that includes a lot of minimum wage workers.

It’s like saying “the median worker should be able to afford a median private jet”. That’s obviously an exaggerated example to make a point.

First you write:

“I don’t get why people think a median worker should be able to afford a median home. Those two medians (worker and home) are entirely unrelated. ”

Then to “support?” this view you write

“It’s like saying “the median worker should be able to afford a median private jet”.

Sorry, this logic is a non starter. If there are homes for everybody then logically the median home price correlates with the median income. This assumes that the buy/rent equation is in balance.

And then you’re correlating house affordability to jet prices?

Seriously?

He is in favor of the Lord/serf economic model of the 1200’s.

MarkinSF,

Yes, jets, to make a CONCEPTUAL point.

“If there are homes for everybody then logically the median home price correlates with the median income. This assumes that the buy/rent equation is in balance.”

You have to make a ton of assumptions for that logic to be accurate, including that everyone from the lowest earner on up should be able to afford to buy. That way you’d have a shot at the two distributions lining up, so the medians would line up. Of course that’s not accurate. Right away you’re slicing off probably/maybe 25%+ of the entry-level (or near) workers from ownership because they simply earn too little to own, period. And then there’s supply. We know there aren’t as many homes as there are people who would like to own them. That’s what rentals are partially for. Not is just some mean capitalist country, but pretty much the entire world.

Now picture those two distributions. The median of homes will be well above the median of worker income. That’s just how it is.

And I’ll add… some will chime in “yeah, but it USED to be that median income afforded a median house”. Yes, I bet that was when demographics and income distribution were very different.

I’m not saying the two medians not matching up is a good thing or a bad thing. I’m just trying to explain WHY they don’t match up, and shouldn’t be expected to.

Nonsense. We have affordability as something that is and has been tracked.

But as a median worker i should be able to afford a median private jet as nice as all the other median work private jet owners. It would only seem fair??

People’s expectations of a starter home have changed dramatically. Our first house was a 1,200 square foot, 3 bedroom/1bath ranch house on a slab with a one car garage. Formica countertops. Sheet vinyl kitchen and bath floor. 12×12 vinyl tile everywhere else. Vinyl cove molding for the wall to floor. No central air. Metal door jambs with slab doors. Closets the size of a suitcase.

You likely couldn’t give that house away today. Everyone wants the HGTV dream home for $1,200 a month, with a pool, 3 car garage, granite, hardwood floors, 3 spa-like baths, and an ocean view. Don’t forget the Viking range and 42″ built in refrigerator.

Lol, I don’t even…

There are plenty of homes. It’s just that many are empty “investment” vehicles. While other people squat those investments or live on the street. Perhaps someday coming to a sidewalk or empty home near you.

El Katz, many many people would be very happy with that starter home you describe. They can not afford it. One of the the biggest groups of buyers of RE recently have been investors. Since around 2012 or so. Even they look for those homes, but not in a downward cycle.

It’s possible that those in your circle don’t like them, but that is not the case for most.

Lynn:

Do read some of the real estate rags regarding current first home buyers and what they are looking for. They want their parent’s house and won’t step down one iota.

Dunno where you live, but I doubt that there’s a long line of peeps signing up for that slab ranch. If so, cities like Wheeling, WV wouldn’t have $25K houses going unwanted. There’s a site “cheapoldhouses” or something along those lines….. many cities have homes you can buy for a buck. Are they broken? Absolutely. Fixable? Yep.

I have a tendency to buy distressed homes in schmancy neighborhoods. I buy the ugly and broken. Someone told me, a long time ago, to buy the smallest and homeliest house in the best neighborhood you can afford. That we did.

Why did I do this? It’s my hobby – I find it much more interesting that golf (which is among the stupidest games ever invented) Most people look at repairs as “erma gerd!”… I look at them as a challenge. My spousal unit tolerated it for several decades because she always marveled at where we ended up when it was complete…. we simply bought junk and fixed it. It may have required that we live in two rooms for awhile (the current house, we had our kitchen stuff all over the living room for 6 months), but at the end of the day, they were showplaces that, when we were done with them, sold quickly.

El Katz, we’re talking two different languages- WV and Ca,. Three actually, you mentioned real estate rags..

WV is probably the cheapest place to buy a home in all of the US. People are not moving there in droves. Although, if I was a republican I probably would.

All of the west coast, where I consider “home” is so overpriced that many people would be more than happy to buy a place like the one you describe. If they could afford it. Same in many less expensive places like Ohio where a friend of mine lives. The people who want to just can not afford it.

Oops, posted in the wrong spot, sorry for double posting..

El Katz, also, distressed homes are a whole other ballgame. I’m looking for one out of necessity but I know how to fix things. Most people don’t. And out of the people who don’t, only those who are naive are going to buy one to live in because they don’t understand the costs of repair. What you are buying is a specialty thing. I doubt you could find much that would be worth it in an expensive market like the west coast right now.

Alan Greenspan had nothing whatsoever to do with any tax rates.

El Katz, also, distressed homes are a whole other ballgame. I’m looking for one out of necessity but I know how to fix things. Most people don’t. And out of the people who don’t, only those who are naive are going to buy one to live in because they don’t understand the costs of repair. What you are buying is a specialty thing. I doubt you could find much that would be worth it in an expensive market like the west coast right now.

Laurence & others,

Agree re the ‘what even is normal’ sentiment…

I’m 32 and am fortunate to have a 2.7% mortgage – but I truly believe interest rates won’t be this low again even in my lifetime.

One thing that the last couple of decades has taught us is that anything is possible and unprecedented things happen all the time – quite frequently in fact.

Some European countries already had negative interest rates and 0% mortgage rates so there’s really no good reason to believe that 2.7% is some sort of ultimate lower bound.

Just as easily nominal house prices could crash by 50% or more or inflation could peak at 20% or more.

Basically, all bets are off. To anyone who says otherwise ask them to show you written dated evidence of their advance predictions of HB1 and GFC, giant bailouts and infinite QE, the pandemic and extreme excessive fiscal stimulus etc.

Just like no-one will predict the next black swan and its unanticipated impact on the world’ financial system.

You may be one of the least dazed and confused commenters on this site.

32 and you own a house? No way (if you listen to the whiners)!

Most people can find a house… once you join the “property ladder” you can eventually get the house you desire.

Obviously, you’ve done it. Both my kids did it. Ain’t rocket surgery. Just takes balls and compromise.

Sure — that and no divorces, illnesses or deaths, PTSD, addiction, job loss/pay cuts or other myriad setbacks.

“balls & compromise“…better trademark that & all other iterations of it (testes & settling-for-less, etc.). Then order up a few thousand t-shirts & bumper stickers. It really captures the spirit of…buying a house.

Actually, you’re not fortunate. You got taken by the financial system and you’ll likely pay somewhere in the future. Let me explain, but the basic summary is this: you can always refinance an interest rate (if rates go low), but you can never refinance the principal (if the house value goes down). Therefore, *for a given monthly payment*, it’s always better to have a higher interest rate with a lower principal than the reverse. You have the reverse.

The only way you come out ahead on this is if you hold your home for 15 or 30 years (i.e. fully paying off your mortgage). And even then, when you eventually sell your house — even if it’s 50 years from now — you will make less money since your initial purchase price was so high.

But you’re 32, and lots of life events can happen. Marriage, kids, divorce, job loss, illness, even good things like a new job you like but that requires you to move to a new state. If any of these events happen to you, and you need to move while you still have a substantial mortgage left during a time when interest rates are high (like now), most likely you will be underwater on your mortgage because your house price will have declined below the remaining principal on your mortgage. Not only can you lose your entire down payment, but you can end up on the hook for hundreds of thousands more to make up the shortfall to your bank, or else declare bankruptcy and endure 7-10 years of credit history hell to get out of it.

IOW, that 2.7% mortgage is like a pair of golden handcuffs: it’s a deal that caused you to overpay on the price of the house, and now, you will never be able to renegotiate that price (like you could an interest rate), and your only hope of this not ending in disaster is that you manage to pay off enough principal through the years of paying down your mortgage such that if/when a life event happens that requires you to sell your house, the principal you have remaining to pay is less than the reduced price of your house.

I don’t mean to wish you ill, and I hope everything works out for you. But I just want people to stop swallowing the real estate industry’s BS spin that somehow every time, any time, no matter what, is always “the best time to buy!”

You didn’t get a deal, and you’re not “fortunate” unless you think the person who sold you that house and walked away with a fistful of equity now converted to hard cash, is somehow *un*-fortunate.

I should have said “normal-ish.” I don’t obviously have an exact line = normal. Sometimes there is an undershoot involved, and sometimes there is not. In Japan’s housing market, after their huge bubble in the 1980s, there was no undershoot. There was just a very long tedious trip back to normal.

Goldman recently released a chart showing that 99% of mortgages have a rate lower than the current 7% rate.

This dynamic is going to create some short, intermediate, and long term effects that are going to be difficult to predict. It could be many years before we reach anything resembling “normal” in the housing industry.

Plus add on the climate change inflation such as the billion in weather damage in CA these last two weeks, the $52.6 billion NY stated they need to deal with climate change costal storms this week, shelter inflation isn’t going backward for many years, if ever, depending on how fast the future changes on many levels.

I agree that 7% mortgages drastically hurt sales, yet there is a lot of inventory that will not enter the market until rates drop substantially as many folks are “locked in” and can’t afford to lose their 3-4% mortgage rates. Thus for mortgage free sellers and buyers in prime properties, the market may hold up much better than expected. The next few years are going to be volatile and tricky for both buyers and sellers, and luck will play a very large role.

Looking at Goldman’s chart, I’m shocked how many conventional 30 year mortgages are locked at 3% rates:

https://pbs.twimg.com/media/FqKwsmvWwAYbbhl?format=png&name=small

With locked in homeowners, the market could see more single unit house rentals hit the market as some people will hold those primary properties at 3% and rent them out, and buy a secondary property to live. Could be a good time to rent a very expensive home on the cheap. I did that twice during the last housing bust, one being a large three story waterfront home in which the developer was in trouble and I was just required to pay the property taxes and keep the utilities paid.

What I think would be very difficult for housing is if/when an “unemployment recession” occurs, as the 8-12 month short sale process delay will start at that moment, and short sales drop all resale values fast. Thus beware that 8-12 month lag “if” unemployment goes up substantially if you are a seller.

The irony is a lot of the inflation volatility has been caused by the low rate mortgages caused by the Fed MBS purchases, which allowed homeowners to borrow hundreds of thousands of dollars per family across the entire county. In simplest terms, money just appeared in their bank accounts like magic with absolutely no productivity, creativity, or labor required. The outcome was obvious, “something for nothing” does have consequences, no matter how delayed the effects.

For example, a new Zillow survey found out that 48 percent of homeowners younger than 40 have tapped their home equity in the past two years, mostly for home improvements. Yet 90% of those homeowners have YET to spend all the money the borrowed, which means there is plenty left for 2023, and all bets are off for 2024 unless the Fed folds and creates an even bigger mess for 2025…TBD…

The Fed helped create consumer immunity to higher prices, and thus has taken away a lot of their strongest monetary powers from to control inflation. So I’d be shocked if they plunge into the ZIRP and QE infinity rabbit hole anytime soon, and if they do, it won’t be for very long as inflation will return with a vengeance like happened in the 1970s.

To steal from Churchill, the Fed is truly “a riddle wrapped in a mystery inside an enigma”, so good luck attempting to figure out the future beyond a simple coin flip…

“…yet there is a lot of inventory that will not enter the market until rates drop….”

This explains low realtor commissions, but not low inventory. People need to stop regurgitating this, in terms of inventory, for which it’s logically incorrect Why? Because:

When a homeowner sells the house they live in, they then have to move into something else, and end up buying something else. So: 1 house comes on the market and 1 house is taken off the market and the net effect on inventory is zero (+1-1=0).

Only Realtors benefit from this because they’re making commissions off both sales; and Wall Street firms benefit from it because of mortgages, MBS, fees, etc. Inventory doesn’t benefit at all.

The only events that increase inventory are these:

1. vacant homes that are now held off the market are put on the market (this can be hundreds of thousands of homes that show up suddenly).

2. Homeowner dies or moves to nursing home or moves to a rental or moves to another country to retire more cheaply, or moves in with kids/parents, etc. and the home is put on the market, and no home is taken off the market.

3. New homes are being built.

Wolf,

I know it is implicitly included in your 1-3 list, but I would just amplify on the looming increase in apartment supply (which, please sweet Jesus, let come to full fruition per reports).

Actually, it would be great to get a monthly post as this supply actually hits the market in various metros…the industry sites have all been reporting on it for 8-9 months, but there is less coverage of the promised supply actually hitting.

That is a good piece of info on the under 40s home equity tap… thanks for those numbers and info.

If it’s a 2nd, money is in the bank. If a HELOC and not drawn out already, the bank can and will reduce those lines. Happened to me in 2009.

Our conundrum is that we will likely consolidate three households onto one property….. the main house goes to the youngsters because they’re fancy-like….. the secondary house goes to the prosperous geezers (me and the spousal unit)… and the ADU goes to my sister who had a medical setback. So, three houses down to “one” (as it’s sold as one property, despite having three dwellings). My son’s spousal unit has a mother that has bupkus… so there might be a second ADU built on the property and 4 turn into one.

The benefit of *not* living in a cliff city.

Thanks, Wolf.

I really respect your opinion. I could easily imagine this being a Japanese-style economy. I’m thinking of this as a secular event (one or more decades). No quick fixes to this one, as the financial engineers and central planners have exhausted most of their ammunition via increasing micro-management since 1987 (Greenspan), in my view. That is, the intervention card has been waaaay overplayed when there was no reasonable (history-based) justification to do it, and now that set of tools is wasted and exhausted.

As I’ve said a few times now, my take is still optimistic, because I think the failure of the central planners is the other side of the coin of the recovery of the unmanaged market economy.

(I’m assuming that Marxists don’t take over Washington…. Marxists wreck everything they touch, and the only fix for Marxism is total systemic collapse. But that is another topic entirely, and I don’t think the US is going Marxist, at least not at this juncture.)

Considering there are zero “Marxists” currently in Congress, I don’t think we are in any danger of them “taking over” any time soon.

“Main Street entrepreneurs.” Nice one Laurence. That was me at age 14. And for the 43 years thereafter. Now that I’ve been retired for a few years, my philosophy is to live within one’s means and enjoy life, each and every day.

Where I live, in Minneapolis’ Longfellow neighborhood, nice, classic Craftsman-style older homes in the mid-$300k range are still selling. $240 per square foot, give-or-take, seems to be the number.

Congratulations, Prairie Rider.

I’m “only” 8 hours north of Minneapolis (in Kenora, ON), and I’ve spent some time in those craftsman neighbourhoods. I enjoyed running the back laneways and pedestrian paths in the summer months….

My prediction is that incentives will again favour self-made entrepreneurs, obviously not the “same” as before, but with an edge over “failing” Wall Street, “once again.”

Those sellers are not just “sittimg on their properties”. They have to pay insurance and taxes on them. Pretty soon, you’ll find lots of keys under doormats. And maybe, for Gen-Z’ers a little note with a smiley saying “sorry”.

Sadly in CA many are paying artificially low taxes thanks to Prop 13

Only if they’re older folks that have lived in their homes for years and years. Not the younger generation of buyers, they’re on the hook for monster taxes in CA, in fact around $12,000-$15,000/yr for every $1 million dollars in assessed value. Think about that. I see homes around the South Bay area selling for $2-$5 million dollars, and I then I get to go back and look at property taxes. I don’t know if its hilarious or just sad at this point, but we have people here buying “average” price homes that pay $20,000-$50,000/year in TAXES alone. FOREVER.

Tell me again how that’s “the American dream”?

John G,

$20-$50k…” Hear ya. The only thing worse would be if CA could mark homes to market. Then ALL homes in that price band would pay taxes that high, rather than just recent buys.

But hey, prop tax looked crazy high like that when my dad bought his house around 1980. “OMG, $2k in annual taxes forever!” Now he pays around $3.5k. So maybe $20-$50k won’t look so bad a ways down the road!

Take a peek at Ill-annoys: My sister had a $500K house there (11 years ago) and the property taxes in Will County were $17K a year. Can’t imagine what they are now.

You could argue they’re artificially low, or you could argue that recent buyers’ are artificially high.

Prop 13 primarily benefits commercial RE and huge multifamily complexes that are held as LLCs or incorporated so the owner of record for tax purposes hasn’t changed for decades and never will until the law changes.

The main effect on single family neighborhoods is a severe “graying” of the population, since empty nesters have no incentive to downsize and end up staying in huge homes well into their 80s, while local schools shutter and the young families that are around often live in cramped apartments.

The passing of prop 19 in 2020 will eventually lead to repeal of prop 13, since it made it much more difficult to pass down the 70s-era tax bases to heirs in perpetuity. Many voters who would have had an incentive to support the current regime now have an incentive to reform it. Those who pay high California sales & income rates will be less and less inclined to give large property tax breaks to a smaller and smaller group of longtime land owners.

“Prop 13 primarily benefits commercial RE and huge multifamily complexes that are held as LLCs or incorporated so the owner of record for tax purposes hasn’t changed for decades and never will until the law changes.”

That’s not exactly correct. When entities such as corporations or LLCs own real estate in California, the real estate is subject to reassessment if there is a “change in control” of the entity that owns it, either directly or indirectly. An entity can own real estate for a long time, but you can’t use an entity to effectively transfer ownership to another party and avoid reassessment. The Revenue and Tax code defines what constitutes a change of control for property tax reassessment purposes.

Remember, not the whole country is experienced bubble prices like the hot markets in California, Texas, Florida. Sure they have gone up but not as much. Thus some areas are not going to drop as much in prices. I would argue that these flyover places where undervalued versus inflation over the past 20 years.

During the peak last year, I read an article that stated that a person who bought a home in Los Angeles in 2020 is sitting on a growth of 800k of equity growth. Of course, this has dropped over the past several months.

But in contrast, a person who bought in Kansas City in 2010 is only sitting on $100k of extra home equity growth.